The IRS recently released a draft of the 2026 Schedule A. The new version jumps from one page to two and includes individual lines for Other Itemized Deduction items. The draft also alludes to new worksheets to calculate the limitation on charitable contributions and the new overall limitation on itemized deductions.

The more things change…

Much of the first page of Schedule A remains unchanged from previous years. There are no material updates to the medical and dental expenses on lines 1-4, or to the taxes paid on lines 5-7. The increased state and local tax (SALT) limitation has received its first inflation adjustment since the passage of the One Big Beautiful Bill Act, as reflected on line 5e. For tax year 2026, the maximum SALT limit is $40,400 ($20,200 MFS). AGI phaseouts are also higher this year than in 2025. Taxpayers will see their SALT deductions limited once their adjusted gross income reaches $505,000 ($252,500 MFS).

The $750,000 limit on acquisition debt is permanent, and the deduction for interest on equity debt has been eliminated. Mortgage insurance premiums are back on Schedule A. The deduction is available to taxpayers with AGI below $100,000 ($50,000 MFS) and is reduced by 10% for each $1,000 ($500 MFS) of AGI over the threshold. The deduction is completely phased out at $109,000 ($54,500 MFS).

Double the Fun

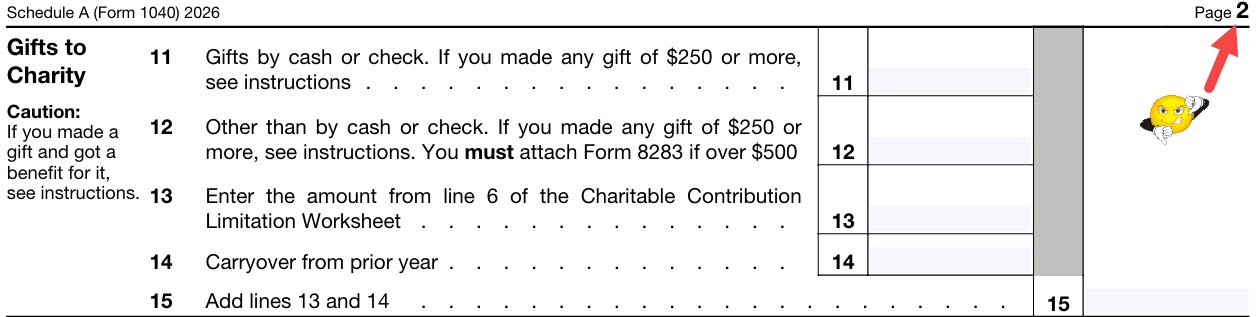

Charitable contributions are pushed onto page 2 of the draft. 2026 introduces a new 0.5% AGI floor for charitable contributions, but the draft contains some surprises in lines 11-15.

As the form is currently designed, the taxpayer reports their total cash and non-cash donations, which are then carried to a new worksheet where the limitation will be calculated. The result of the worksheet is then entered on line 13 of Schedule A. Line 14 reports carryovers from previous years. While the code contains nothing indicating that pre-2026 carryovers are not subject to the new floor, the form’s design suggests these amounts will not be subject to the 0.5% haircut. It is important to remember that the form is just a draft and that there may be changes before the final form is released. Keep in mind that the IRS can take a taxpayer-friendly position if they choose (but don’t hold your breath). We will have to wait to see what the final form does and how the limitation is applied when the worksheet is released.

For tax year 2026, the charitable contribution deduction for nonitemizers’ returns is not subject to the 0.5% limitation. Qualified charitable distribution (QCD) also escapes the chop, so for eligible taxpayers (even those who itemize), QCDs may offer more tax benefits this year than in the past.

Line 16 is where allowable casualty and theft losses arising from a disaster are reported. Personal casualty losses remain nondeductible unless in the case of a federally declared disaster. Beginning for tax year 2026, losses from certain state-declared disasters will also be deductible.

Line ‘Em Up!

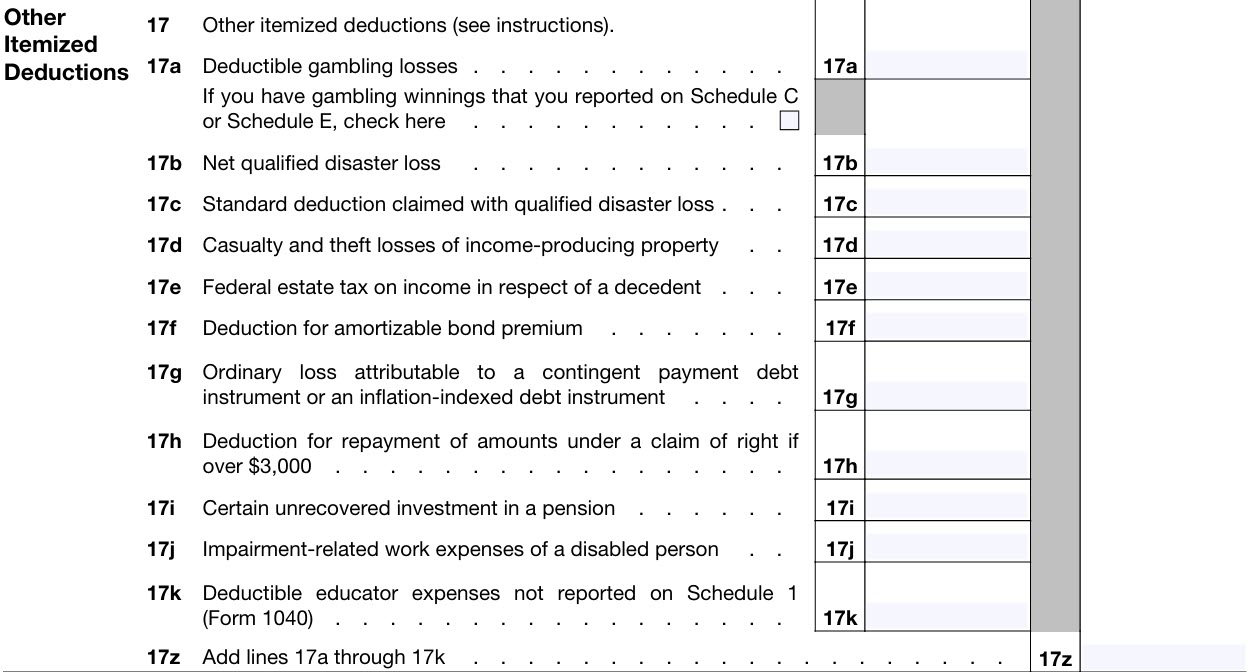

In previous years, any items falling under “Other Itemized Deductions” would be listed on line 16 of Schedule A. The 2026 draft form adds 11 detail lines, expanding this section from line 17a through 17z.

OB3 added a new limitation to gambling losses, which means the amounts reported on line 17a might be lower than in the past. This new limit is applied before the “to the extent of winnings” limit, so once all the wagering wins and losses are totaled up, only winners or break-even gamblers will feel this change. There is also a new checkbox to indicate whether the taxpayer has gambling winnings reported on Schedule C or Schedule E. Taxpayers who gamble frequently may want to use the daily netting strategy we discuss here to avoid paying tax on phantom income.

Losses from qualified disaster losses are reported on line 17b. Qualified disaster losses are individual casualty or theft losses that are attributable to a Presidentially declared major disaster, and that fall within specific statutory time frames. These losses are treated more favorably than ordinary casualty losses. They may be claimed either as itemized deductions or as an increased standard deduction, and they are subject only to a $500 per casualty floor with no AGI reduction. If the taxpayer is claiming the standard deduction with the loss, that is indicated on line 17c.

If a taxpayer experiences casualty or theft losses of income-producing property, those are reported on the new line 17d. Individuals from all walks of life have been targeted by scammers looking to get their hands on retirement funds, digital asset investments, or bank account balances. While it is always sad, it is not always deductible. The IRS Office of Chief Counsel issued CCA 202511015 describing the scenarios that would lead to deductible losses. Click here to read a deep dive on our analysis of these “investment theft losses”.

Lines 17e-17j list out the old favorites from the other itemized deductions: estate tax paid on income in respect of a decedent, amortizable bond premiums, losses from contingent payment debt instruments or inflation-indexed debt instruments, claim of right repayment deductions, unrecovered pension investments, and impairment-related work expenses.

The last new item on the list is on line 17k, where amounts exceeding the $350 educator expenses limit from Schedule 1 are deducted.

Once all itemized deductions are totaled, the taxpayer must determine whether they are subject to the new overall limitation on itemized deductions, which appears on line 18. Taxpayers with taxable income (without factoring in itemized deductions) in the 37% tax rate will only get 35% worth of benefit from their itemized deductions. The new line states that any taxpayer with income above $384,350 (the threshold at which MFS hit 37%) must complete the itemized deduction worksheet (not currently available) to determine their allowable deductions.

This threshold is obviously far lower than the 37% threshold for a single taxpayer. We believe that to reduce the amount of information that appears on Schedule A, the IRS opted for the lowest possible threshold for which the worksheet may be needed. Just because this box is checked “yes” doesn’t mean the taxpayer will be limited.

As the instructions are issued later in the year, many of the open questions will hopefully be answered, and we will address them all in our Update for 2026 Returns seminar.